Decomposition of Disaster Region using Earthquake Parameter and STDM Distance: Catastrophe Bond Pricing Single Period

DOI:

https://doi.org/10.37934/araset.43.1.171200Keywords:

Regional decomposition, Earthquake disaster, Disaster bond pricing, EDRI, Earthquake parameters, STDM distanceAbstract

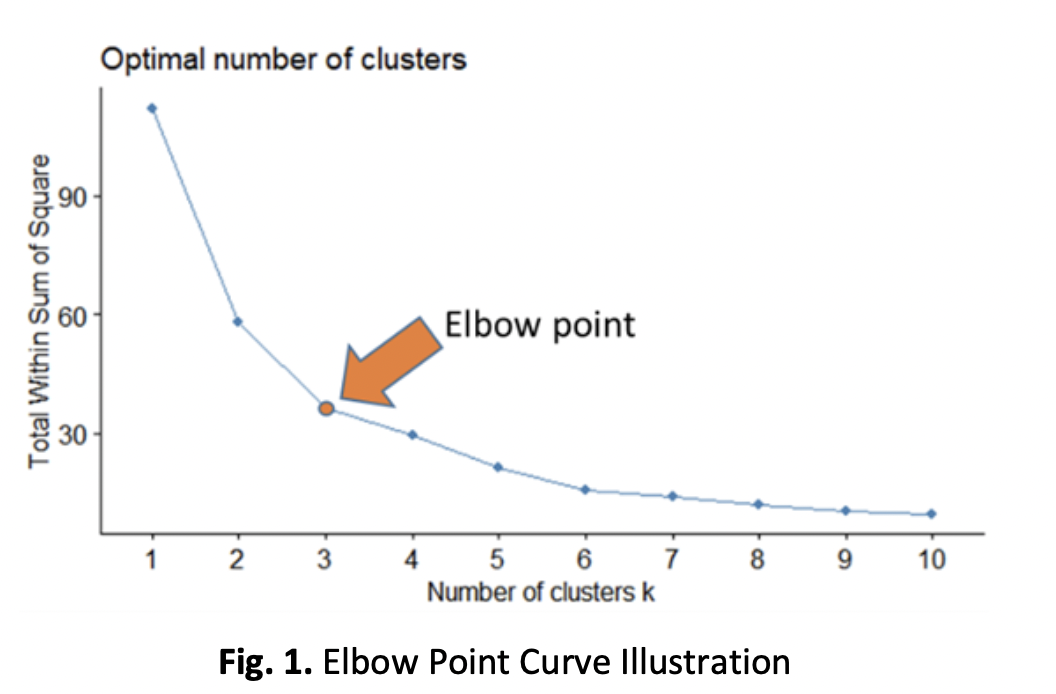

Investor interest in single-regional earthquake catastrophe bonds has the potential to decline in the future. To pique investor interest, disaster bond prices can be determined by decomposed disaster zones using seismic parameters and Space Time Depth Magnitude (STDM) distance. Therefore, this study aims to develop a Decomposition of Disaster Region Using Earthquake Parameters and STDM Distance on the Earthquake Catastrophe Bond Pricing (DECBP) model for a single period. The basic idea of developing the model is to observe earthquake characteristics in an area by clustering the area based on the Earthquake Disaster Risk Index (EDRI), earthquake parameters (earthquake magnitude and depth), and STDM distance. The research and development (R&D) methodology used in this work is pursued through the creation of a mathematical model for calculating the price of earthquake catastrophe bonds over a single period. The development stages carried out are regional decomposition modelling, payment functions modelling, distribution of extreme earthquake magnitude values modelling, prediction of interest rates and coupons, numerical simulations, and analysis of the effect of interest rates, coupons, and the amount of regional decomposition on earthquake bond prices. Interest rates, coupons, and the number of regional decompositions that affect bond prices for earthquake events are the results of the analysis of the model that's been developed. The resulting model in this study is expected to assist the Super Purpose Vehicle (SPV) in determining the price of earthquake bonds and serve as a reference for future researchers developing models for the price of earthquake catastrophe bonds.

Downloads

Downloads

Published

How to Cite

Issue

Section